Is it better for you to buy Index Funds (or ETFs), instead of investing on your own?

Is it better to just buy Index Funds (or ETFs), instead of investing on your own (in individual stocks)? This is a question that I hear frequently. I'll answer this important question right now, let's get started...

Trillions have gone into index funds

According to Morningstar during the past 10 years, investors have pulled about $1.4 trillion from active U.S. stock funds, with most of the money — $1.3 trillion – going to passive funds (Index and ETFs).

What is an Index Fund?

An index fund buys the stocks that make up an entire index (list). For example, if the index tracks the Standard & Poor’s 500 — a list of 500 of the largest companies in the United States — the fund buys shares from every company listed on the index. You, in turn, buy shares from the index fund, whose value will mirror the gains and losses of the index being tracked.

What is an ETF?

An exchange-traded fund (ETF) is a type fund that owns a collection of stocks—that tracks an underlying index. ETFs are essentially similar to index funds; however, they are listed on exchanges and ETF shares trade throughout the day just like ordinary stock.

What is Individual Investing?

Individual Investing or the Simply Investing way, is to invest in individual companies (stocks) that are both quality companies and are undervalued (priced low). Any company that passes my 12 Rules of Simply Investing is a quality company that is also undervalued. Our focus is not on stock price appreciation but on creating for yourself a reliable stream of growing passive income, that you can use to cover all your expenses. Using this approach, some people have retired from their day job in their 30s, or 40s, it all depends on your personal level of expenses and lifestyle. Even if you love your day job and never plan to retire, a growing stream of passive income gives you opportunities, opportunity to travel, support great causes, support your family, reduce your workweek, and hundreds of other options that become available when you are financially free.

What about investing in startups, cryptocurrency, new technologies, high-growth companies?

You can invest in startups, cryptocurrency, new technologies, high-growth companies, if:

- you are very knowledgeable in those industries

- you have the time, resources, confidence, and expertise to research those industries

- you understand and accept the risks of investing in those industries

- you can absorb any financial losses that you may incur by investing in those industries

But, before you decide to invest in startups, cryptocurrency, new technologies, high-growth companies, you must:

- build for yourself and your family a solid investment portfolio that provides you with a reliable stream of growing passive income

With a reliable stream of growing passive income, your living expenses and lifestyle are protected, only then should you venture out and make higher-risk investments if you wish. There are no shortcuts, it takes time to build a reliable stream of growing passive income. With this approach you need two things: time & money. The younger you are, the more time you will have to build a solid income-producing portfolio. The more money you have, the bigger the portfolio you will be able to build for yourself. Having both time & money is even better!

Vanguard Index Fund vs Individual Investing

A reader asked about the difference between just buying Vanguard Index Funds (VYM, VOO, VYMI) versus investing on her own. Which is the better approach? In order to answer her question, I'll cover the following topics in this article:

- With Vanguard (or any other Index Fund or ETFs) you are still paying fees

- With Index/ETF funds you are inadvertently buying overvalued stocks

- With Index/ETF funds you are inadvertently buying non-quality stocks

- With Index/ETF funds your dividend yield is lower

- With Index/ETF funds you'll eventually have to start selling your shares

- Unpredictable dividend income from Index/ETFs

- Over diversification is a problem

- Benefits of investing in dividend stocks

- Index Funds are best for this type of individual

- Pros & Cons

#1: With Index/ETF funds you are still paying fees

The fees for Index Funds and ETFs are much lower than fees for actively managed mutual funds, but there are still fees to be paid by you. If you are investing small amounts of money the fees may seem insignificant, but when you start investing $100K, $300K, $500K or over $1M, the fees will start to negatively impact you.

Let's have look at the fees:

- Vanguard High Dividend ETF (VYM): 0.06%

- Vanguard S&P 500 ETF (VOO): 0.03%

- Vanguard International High Dividend (VYMI): 0.32%

I used the following values to determine the fees for each of the funds:

- Total invested: $200,000

- Investment held for: 20 years

- Front end sales fee: 0%

- Past return: 13.8% (Vanguard S&P 500)

I used the following online calculator: https://www.getsmarteraboutmoney.ca/calculators/mutual-fund-fee/

Fees paid after 20 years:

- VYM: $11,488.33

- VOO: $5,743.25

- VYMI: $61,356.19

- Individual stocks: $175

Most online brokers charge a trading fee of $5-$10 for buying/selling individual stocks, with $200,000 you could buy 35 stocks and your cost over 20 years would be $175

By the way; $500,000 invested for 25 years in VYM would cost you $57,068.32 in fees.

#2 With Index/ETF funds you are inadvertently buying overvalued stocks

Let's take a look at the number of companies (stocks) held in each of these funds:

- VYM: 406 companies

- VOO: 511 companies

- VYMI: 995 companies

On any given day not all of the companies in these funds are going to be undervalued (priced low). From the Simply Investing Course you understand the importance of buying quality stocks when they are undervalued (priced low), remember:

- A stock is undervalued when it’s current dividend yield is higher than its average dividend yield:

- stock is undervalued (priced low) if current dividend yield > average dividend yield

- stock is overvalued (priced high) if current dividend yield < average dividend yield

When you buy an index fund your money goes to buying both undervalued and overvalued stocks.Therefore you are inadvertently buying stocks that are priced high, those stocks have limited potential to go up even higher since they are already priced high, in the long-term this will negatively affect your portfolio's performance.

#3 With Index/ETF funds you are inadvertently buying non-quality stocks

From the Simply Investing Course you understand the importance of investing in quality companies, companies that:

- are recession proof

- provide essential products & services

- have a low-cost lasting competitive advantage

- have a history of profitability

- have a history of paying growing dividends

- have a low payout ratio

- have low debt

- have low P/B, P/E ratios

Basically a company must pass the 12 Rules of Simply Investing in order to qualify as a quality company.

Would you buy a company that had 500% debt, or P/E of 275, or wasn't profitable? If you wouldn't buy even one poor performing company then why would you buy it as part of a larger Index Fund or ETF? With these types of funds your are inadvertently buying non-quality companies.

#4 With Index/ETF funds your dividend yield is lower

Let's take a look at the current dividend yields of each of these funds:

- VYM: 3.16%

- VOO: 1.97%

- VYMI: 4.24%

Now let's take a look at the current dividend yields of a few quality companies:

Enbridge: 6.15%

Simon Property Group: 5.56%

The Gap: 5.52%

AT&T: 5.33%

Power Corporation: 5.33%

BCE: 5.05%

Ryder System 4.67%

TC Energy: 4.52%

The yield for the funds is lower for two reasons:

- they are invested in companies that pay very little dividends (some companies only yield 0.5%)

- in the case of VOO they are invested in some companies that don't pay any dividends

Would you rather earn 1.97% on your investment or earn 5%?

$200,000 invested over 10 years (assuming no stock price appreciation to keep the math simple), with dividends re-invested with a 1.97% yield, you would earn: $43,082.78 in dividends

$200,000 invested over 10 years (assuming no stock price appreciation to keep the math simple), with dividends re-invested with a 5.00% yield, you would earn: $125,778.93 in dividends

In the long-term the dividend yield you earn matters.

#5 With Index/ETF funds you'll eventually have to start selling your shares

With Index/ETF funds you'll eventually have to start selling your shares, especially with funds like VOO, or similar ones that hold stocks in companies that don't pay dividends or pay very little dividends. Your living expenses, vacations, homes, cars, boats, clothing, food, giving to charities, education, healthcare all cost money, you cannot pay for these things with stocks. You have to cover your expenditures with cash, you can only do this by using dividends or selling some of your shares. This becomes a bigger issue the longer you live, if you just need 5, 10, or 15 years to live off your investments you might be fine selling your shares in index funds or ETFs.

However if you need to live off your investments for 20, 30, 40 years, or would like to leave your kids/family with a solid investment portfolio, then selling shares in your index funds could eventually lead to you having to sell off all your shares, resulting in no investment portfolio at all. The situation become worse if we are hit with a recession (or downturn) that lasts 5-7 years. During a downturn you still need to live and pay for things, so you start to sell some of your shares in your index funds, the problem is in a market downturn shares prices are already low (this is the worst time to sell), you end up selling more shares (just to cover your costs), which further shrinks your portfolio.

With individual investing, we do not selling our shares, we design our portfolio to maximize on growing passive income. What happens to the dividend when stock prices drop? What happens to the dividend when there is a recession? The dividend continues to go up. In the last +20 years my dividend income has continued to increase every year, and you can take a look topic #6 to see the consecutive years of dividend increases for a number of companies.

#6 Unpredictable dividend income from Index/ETFs

The Vanguard High Dividend Yield ETF (VYM) is invested in more than 400 companies – certainly not all of their dividend payments will be safe throughout a full economic cycle.

The VYM fund’s dividend payments were negatively affected during the last recession. Total dividend payments reached $1.44 per share in 2008 before falling to $1.17 in 2009 and $1.09 in 2010, representing a high-to-low decline of about 25%. Annual dividend payments didn’t recover back to their 2008 peak until 2012.

Put another way, if a retired investor owned 25,000 shares of VYM, she would have received $36,000 of dividend income in 2008.

By 2010, her annual dividend income had fallen to about $27,000 – a drop of more than $725 per month. Depending on her budgeting, margin of safety, living expenses, her life could suddenly have become much more difficult.

VYM's price also fell by more than 32% in 2008, likely invoking plenty of fear as the value of her nest egg fell from $1,000,000 to less than $700,000. To be fair, even with individual stocks your prices will drop during a recession. However the key here is not the stock price but the income being generated from your portfolio. With individual stocks you can pick and choose the best reliable dividend companies, to ensure that your dividend income is safe and continues to grow even during a recession. How can you ensure growing dividend income? By focusing on buying companies that have a history of consecutively increasing dividends (below is just a small sample):

| Company Name | Consecutive Years of Dividend Increases |

| Northwest Natural Holding Company |

64 |

| Dover Corporation | 63 |

| Genuine Parts Company | 62 |

| Emerson Electric | 61 |

| Procter & Gamble | 61 |

| 3M | 60 |

| Cincinnati Financial Corporation | 57 |

| Johnson & Johnson | 56 |

| Coca-Cola | 55 |

| Lowe's | 55 |

| Lancaster Colony Corporation | 55 |

| Colgate-Palmolive | 54 |

| Hormel Foods Corporation | 53 |

| Stanley Black & Decker | 51 |

| SJW Group | 51 |

| Target | 50 |

| Black Hills Corporation | 48 |

| W.W. Grainger | 46 |

| Becton, Dickinson and Company | 46 |

| Kimberly-Clark | 45 |

| Pepsi | 45 |

| V.F. Corporation | 45 |

| RPM International Inc. | 45 |

| Walmart | 45 |

| PPG Industries | 45 |

| Consolidated Edison | 44 |

| Illinois Tool Works Inc. | 44 |

| S&P Global Inc. | 44 |

| Automatic Data Processing | 43 |

| Archer-Daniels-Midland | 42 |

| Walgreens Boots Alliance | 42 |

| Pentair plc | 42 |

| McDonald's | 41 |

| Sherwin-Williams Company | 41 |

| Clorox | 40 |

| Medtronic | 40 |

I've been investing the Simply Investing way for more than 20 years, and the income generated from my portfolio has grown every single year.

#7 Over diversification is a problem

Over diversification can be a problem, because when you purchase hundreds of companies (thru an Index Fund or ETF, for example VYMI owns 995 companies) there is a higher likelihood that you will:

- buy companies that overvalued (priced high)

- buy companies that are not quality companies

- buy companies that don't pay dividends or very little dividends

George Athanassakos is a professor of finance and holds the Ben Graham Chair in Value Investing at the Richard Ivey School of Business at the University of Waterloo. Click here to read Professor Athanassakos's view on over-diversification and risk for value investors.

What about international diversification?

People believe that they need to buy international stocks, in order to get global diversification, so they invest in international index funds.

There is international exposure already from large US and Canadian companies that I track in the SI Report, companies like:

- Coca-Cola (operates in over 190 countries)

- Exxon (operates in over 50 countries)

- Johnson & Johnson (operates in over 60 countries)

- McDonald's (operates in over 119 countries)

- Royal Bank of Canada (operates in over 37 countries)

Some large US/Canadian companies now actually earn more money internationally than they do in their home country. These companies have international and local experts to take advantage of growing global markets. Let these global companies worry about trade polices, currency fluctuation, political risk, sanctions, and regional issues. There is no need for you to spend time and resources to research foreign companies to invest in.

The US and Canadian stock markets are some of the most heavily regulated markets in the world, their strict requirements and regulations are designed to promote fair trade. Stock markets in other countries like South America and Asia are much more risky for investors, this is why I prefer to invest in US and Canadian markets.

Another option is to buy ADRs (see explanation below). For example BP (formerly known as British Petroleum) is a UK company but it has ADR shares that trade on the NYSE.

ADR: An American depositary receipt (ADR) is a negotiable certificate issued by a U.S. depository bank representing a specified number of shares in a foreign company's stock. The ADR trades on markets in the U.S. as any stock would trade.

An international index fund or ETF run into the same problems already identified above, but now they expose you to additional risk by investing directly in more (international) riskier markets.

#8 Benefits of investing in dividend stocks

There are 4 main benefits of investing in dividend stocks:

- dividends provide an immediate return on your investment, regardless of stock price

- dividends provide cash in your pocket, you can spend the money if you wish or re-invest it

- once given out dividends cannot be taken back, if your company declines (or goes bankrupt) the dividends you've received over the years are yours to keep

- over time dividends reduce your risk, by increasing your margin of safety, see my example below:

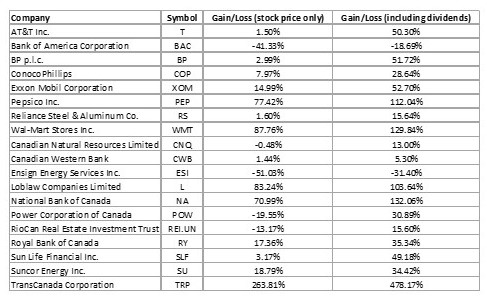

Dividends increase your returns and minimize your losses. Have a look at a few of my holdings and see for yourself the impact of dividends on my returns:

Dividends have allowed me to reverse my losses (CNQ from -0.48% to 13% return), and magnify my gains (AT&T from 1.5% to 50.3%).

Below is another example of 3 stocks I currently own:

| Company | Initial Investment | Dividends Received to Date |

| TC Energy | $2,479 | $6,134 |

| Power Corporation | $7,996 | $8,839 |

| Sun Life Financial | $4,040 | $4,460 |

Notice in the above table that the amount of dividends received so far have exceeded my initial investment, this has effectively reduced my risk to zero with these 3 companies.

#9 Index Funds are best for this type of individual

Index funds and ETFs are best for people who:

- do not have the time or desire to select quality dividend-paying stocks when they are undervalued (even though the SI Report makes this very easy and quick to do)

- do not have the knowledge to select individual stocks (the SI Course makes this easy to do)

- do not have the patience or confidence to invest on their own

PRO Index Funds & ETFs:

- very easy to buy (just call your Index Fund company)

CON Index Funds & ETFs:

- inadvertently buying overvalued companies

- inadvertently buying non-quality companies

- inadvertently buying companies with low to zero dividend yield

- higher fees than investing on your own

- over diversification may result in lower long-term results

- without dividends you are only hoping for the stock prices to go up

- with a low dividend yield, you will have to start selling your shares in order for your portfolio to generate income

PRO Investing on your own:

- very low cost to buy stocks

- no ongoing fees to pay

- you select quality dividend-paying stocks when they are undervalued (priced low)

- with dividends you get paid for owning shares

- provides growing income via dividends so you don't have to sell your shares

CON Investing on your own:

- takes time to select the right stocks (but SI Report makes this very quick)

- you have to learn how to invest (but SI Course makes this easy)

Conclusion

How you invest is entirely up to you, and it depends on your level of knowledge, time, risk tolerance, and confidence. There are so many approaches to investing, but the Simply Investing way helps you to earn more, save time, and reduce your risk.

I have been investing the Simply Investing way for more than 20 years now, and its working for me because it maximizes my gains, lowers my risk, generates growing income every year, and saves me time. Investing does not have to be complicated, focus on buying quality companies when they are undervalued (priced low). Invest now for a richer future tomorrow.

Did you enjoy reading this article? If so, I encourage you to sign up for my newsletter and have these articles delivered via e-mail once a month…and it’s free!

{kind=link}

1 comment

I love this article. I really appreciate the point about the dividends being higher than SPY... not too hard. Your points about international exposure is one that I think people forget to think about

Leave a comment