Fees & Your 5 Common Questions to Investing

If you own any mutual funds, index funds or Exchange Traded Funds (ETFs) you need to understand the impact of those fees on your investments. A tiny fee of 0.08% can cost you thousands of dollars over the long-term. Even when people save and invest diligently over their entire lives in funds, they unknowingly lose thousands in fees, hence they have to continue working past the age of 65 just to get by.

If you own any mutual funds, index funds or Exchange Traded Funds (ETFs) you need to understand the impact of those fees on your investments. A tiny fee of 0.08% can cost you thousands of dollars over the long-term. Even when people save and invest diligently over their entire lives in funds, they unknowingly lose thousands in fees, hence they have to continue working past the age of 65 just to get by.

What fee?

All mutual funds, index funds and ETFs carry fees, the fee is known as the Management Expense Ratio (MER). The MER is used to pay for expenses incurred by the fund company for managing the fund. Even index funds cost money to manage, the fund company needs to cover the cost of staff, offices, IT systems, and marketing.

I don't pay fees, my company charges $0 commission for trading ETFs

The $0 commission is for buying and selling ETFs, and it's great you are able to trade ETFs for free. But the ETFs themselves still charge you the MER fee, which is like a hidden fee, because it's deducted immediately before you see any gains or losses.

Do I still pay the fee if my funds do poorly?

Yes, the MER fees is charged regardless of how well or how poorly your funds perform, let's take a look at two examples (where the MER is 2%):

Example 1: Your funds do really well and gain 5%

Your actual return: 5% - 2% = 3%

Example 2: Your funds do poorly and loose -4%

Your actual return: -4% - 2% = -6%

As you can see from the above examples, in good times your gain is reduced by the fee. In bad times your loss is amplified by the fee.

How much am I paying in fees?

How much you pay in fees depends on the MER, how much you invest, and how long you stay invested. Let's take a look at some examples:

Assumptions:

Yearly contributions, in addition to amount invested: $1200 ($100/month)

Average Rate of Return: 8%

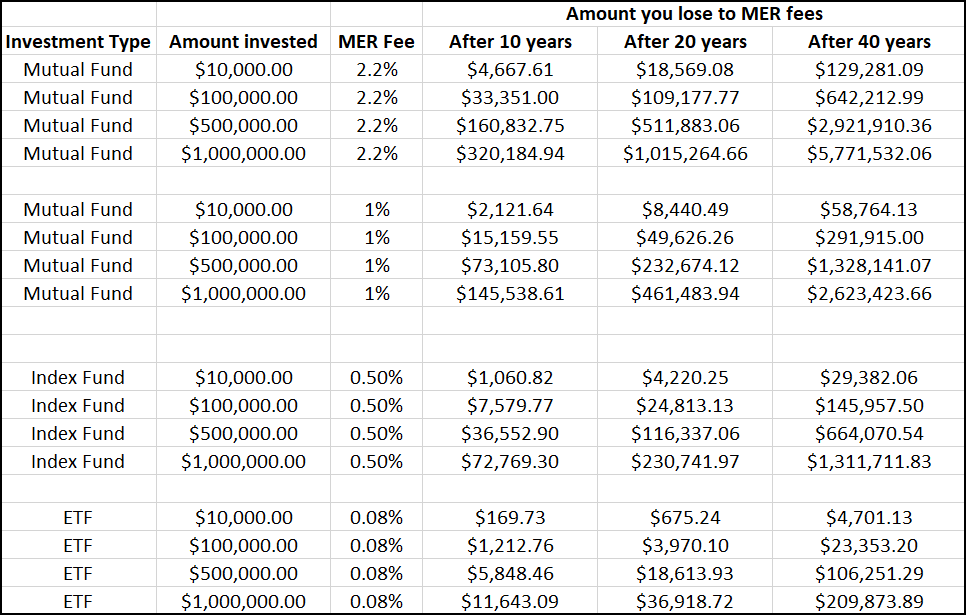

In Canada the average MER is 2.2%, and the average amount held in a retirement account (RRSP similar to a 401k) is $100,000. Therefore the average Canadian over their lifetime could pay $642,212 in fees. I don't know about you but I could sure use an extra $642K.

Don't invest in mutual funds, index funds, or ETFs, instead invest in individual stocks. But not just any stocks, only invest in quality stocks when they are undervalued (priced low). How do you find quality stocks? Just apply the 12 Rules of Simply Investing.

I can help you to start investing today, why re-invent the wheel when you can learn from my 20-years of being in the stock market. I've witnessed first hand the ups and downs of the market, and I know what it's like to start investing your hard earned money. I created the 12 Rule of Simply Investing to help you get started right away, so you don't have to wait on the sidelines any longer. The sooner you start investing the sooner you will be on your path to financial freedom.

Did you enjoy reading this article? If so, I encourage you to sign up for my newsletter and have these articles delivered via email once a month … for free!

{kind=link}

1 comment

Amazing post. Helpful.

Leave a comment